Sustainability aspects in DCF valuation

March 31, 2023

Topics

A sustainably built and operated property typically has a higher market value than an otherwise identical property that does not or only partially meets sustainability requirements (for example, if it is heated with fossil fuels instead of a heat pump). However, investments in sustainable properties are usually higher. This simple comparison alone shows that the influence of sustainability factors on the market value of real estate is complex.

This paper addresses the question of how sustainability aspects, with an emphasis on energy renovations, are incorporated into a valuation performed using the discounted cash flow (DCF) method. In any DCF valuation, the focus is on revenues, costs, and discounting. Each of these three parameters is influenced by factors related to sustainability. A selection of these will be presented here, beginning with the factors that influence property income.

Yields

Investments in sustainability have a wide-ranging impact on earnings. Naturally, the potentially higher rental income is the most important factor.

- Rental income from new leases: Properties heated with a heat pump generally have lower utility costs than those heated with fossil fuels. The current energy crisis – including the sharp rise in fossil fuel prices – boldly underlines how much the heating source can influence utility costs. The C02 tax also has an impact here. For tenants, the gross rent (net rent plus ancillary costs) is decisive. The lower ancillary costs of sustainable properties enable owners to charge a higher net rent.

- Rental income on new leases: In Switzerland, tenants of commercial properties whose sustainability performance is being monitored are willing to pay more.

Rental income from existing tenants: The costs for energy-efficient renovations can be partially passed on to existing tenants, which generally increases the rent. According to Swiss residential tenancy law, the pass-through rate is generally higher when investments are made in sustainable building components during renovations.

Exit values of sustainable building components in terms of the circular economy: Currently, most building components are installed and bonded in such a way that they can hardly ever be reused. However, this will change in the future. There is a growing awareness of this issue and regulations concerning it are becoming increasingly prevalent.

Cost

On the cost side, the main factor is the higher investment required for measures that promote sustainability. However, government funding incentives help to reduce these costs.

- Investment costs for sustainable building technology: Substituting fossil fuels with renewable heating sources results in significantly higher maintenance costs. For example, installing a heat pump is much more expensive than replacing an old oil heating system with a new one.

Accompanying measures: How much higher the repair costs turn out to be for a heating system replacement depends on whether further investments (such as additional insulation measures, underfloor heating, photovoltaics, etc.) are necessary.

Subsidies: Incentives reduce the costs of sustainability investments. - Operating costs: Sustainable properties, and particularly renewable heating sources, typically generate lower operating costs. These savings pay for themselves over time.

Service life of sustainable building components: Sustainable building components are characterized by a longer service life. This means that major maintenance and repair costs can be saved over the entire life cycle.

Discounting

A lower expected return results in a lower discount rate, and this leads to a higher price in a DCF valuation.

Discounting/expected return: Investors are more willing to pay for sustainable real estate. Accordingly, they accept a lower return for owning a sustainable property than a non-sustainable one. Since renovation reduces the risk of a property becoming a stranded asset, the discount rate after a refurbishment may be lower than before.

Recent empirical study

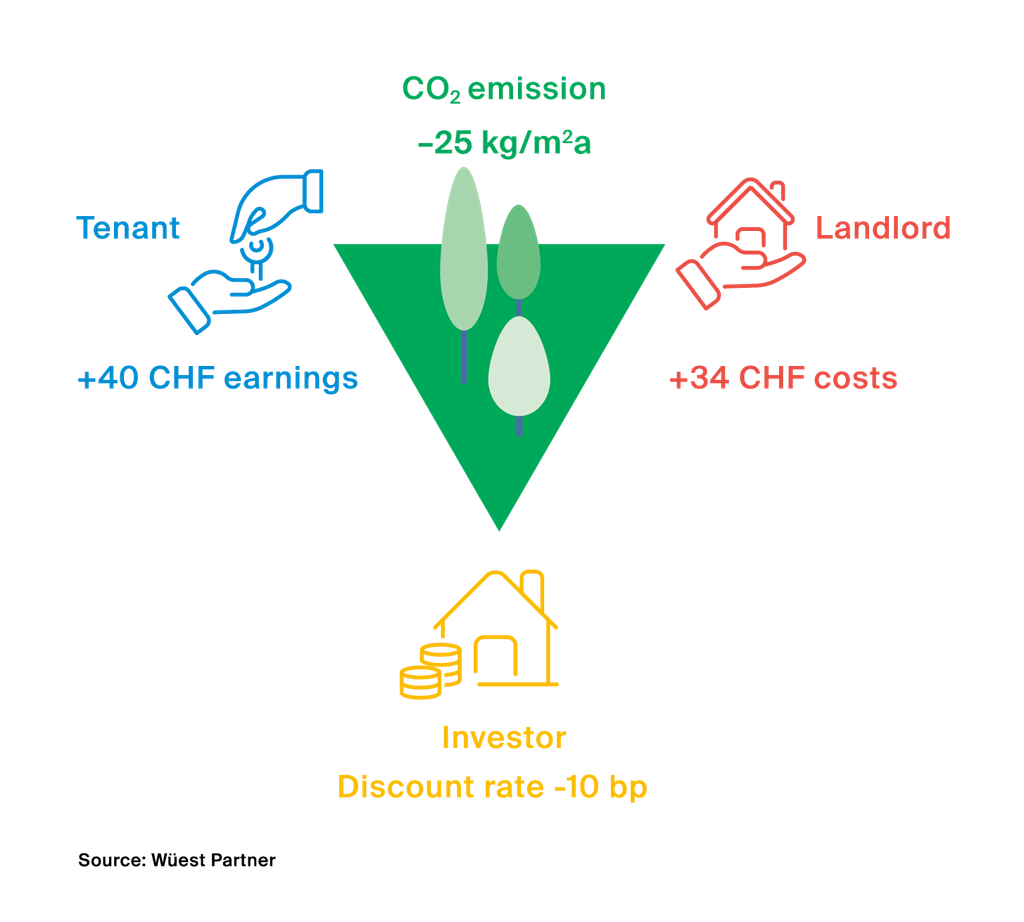

A recent study by Wüest Partner provides information on the magnitude of such sustainability effects for Switzerland. Based on data from 2015 to 2020, the results are summarized in the graphic and text below.

Economic viability of an energetic renovation

As a result, an investor pays on average around 4 percent less for an otherwise identical apartment building that is heated using fossil fuels than for one that is heated sustainably. The net rent of a rental apartment is, on average, 40 francs per apartment per month more expensive in a sustainably heated building. As illustrated above, this is primarily due to the lower ancillary costs. However, the amortization costs for installing a heat pump are higher than replacing an old heating system with a new oil or gas version. Since these amortization costs only increase by 34 francs per apartment and month on average, owners can still expect a small profit. This is why investors accept a 10 basis point lower return for sustainable properties. Incidentally, in many cases the burden on tenants decreases nonetheless, since ancillary costs often fall more sharply than net rents.

You can find out more about this in the study Effect of sustainability on real estate values (German), which Wüest Partner conducted in 2022 with the support of the Federal Office for the Environment (FOEN).

Change and consistency

It is plausible that the willingness to pay for sustainable properties has increased further in the meantime. Finally, the terms “stranded assets” or “carbon value at risk” are gaining importance among investors, and with the energy crisis, tenants are more aware of ancillary costs. In a valuation context, it is therefore important to remain constantly up to date. What has remained the same is that in a DCF valuation, the value-relevant aspects are assessed individually by the valuer. In doing so, it is advantageous to be able to rely on current and comprehensive benchmarks.

Benchmarks and simulations

Supporting the valuation process with substantive and reliable data is an important cornerstone in quality assurance. In order to take sustainability aspects into account objectively and in a value-relevant manner, it is necessary to expand traditional valuation know-how. Wüest Partner makes this possible through internal and external training and knowledge transfer. On the other hand, statistical models (based on artificial intelligence, for example) and comprehensive benchmarks are crucial. This enables data-supported, objective proposals to be made in the valuation process. It also allows the evaluation to be broadly compared and supported. Obtaining quality-assured data to calculate benchmarks is critical in this regard. The more a company anticipates the market, the earlier they can systematically collect and store relevant data. In the area of building materialization, survey apps such as Wüest Visits are invaluable for achieving considerable accuracy in building-level databases (a digital twin). Especially in the area of renovation and the associated maintenance costs, an efficient DCF calculation tool with a high degree of flexibility offers the possibility of evaluating energy scenarios in a wide range of variations with little effort, both from an economic and an ecological perspective.

Outlook

Wüest Partner invests continuously in data and model development as well as knowledge acquisition in order to more accurately reflect sustainability aspects in valuations. For example, we are currently developing a database to systematically record potential subsidies for energy-efficient renovations. The example of the circular economy shows how dynamically the topic of assessment and sustainability is developing: In today’s existing properties, the building components are usually glued together in such a way that recycling is rarely economically worthwhile. Now, however, more and more buildings are being constructed in such a way that their resources can be reused later. Accordingly, an “exit value” of building components could also occur in a few years. The service life of components will also become more important.

A holistic approach

This article focuses on the energy aspects of renovating investment properties. Of course, sustainability is a very comprehensive topic. Other factors, such as the location of the property, are also significant for example, those regarding induced mobility or stranded asset risk. Wüest Partner covers this more extensive assessment of sustainability using an ESG rating, which we primarily see as a tool that provides owners or investors with a holistic view of the property and sheds light on many new aspects. This allows measures to be evaluated comprehensively and strategies to be implemented in their entirety. Objectivity and comparability are of paramount importance to Wüest Partner; the approximately 75 indicators are determined by data and result in an implicit benchmark of the Swiss building stock.