Investment properties in a turbulent market environment

December 15, 2022

Topics

The capital market is in turmoil, inflation is high, and interest rates have reversed. Nevertheless, the prices of investment properties in Switzerland have barely moved from their highest point So why is this?

The impact of the real economy, supply and demand, inflation and interest rates on property prices in the current market environment will be explored in more detail in a series of blog posts. In this article, we focus on the interplay of inflation, interest rates, and real estate prices.

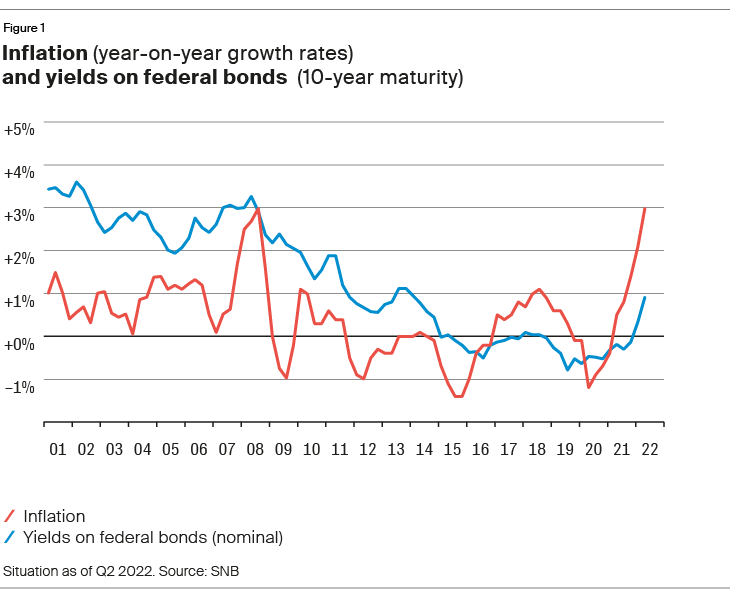

Government bond yields reflect inflation expectations

From an economic perspective, it is clear that a rise in inflation leads to a rise in interest rates, which in turn increases the return expectations of real estate investors. Since mid-2022, the Swiss National Bank (SNB) has upped key interest rates by a total of 1.25 percentage points to a current level of +0.5 percent, with the aim of combating rising inflation. However, federal bond yields, which help determine investors’ inflation expectations over their respective durations, had already risen significantly prior to the rate hike.

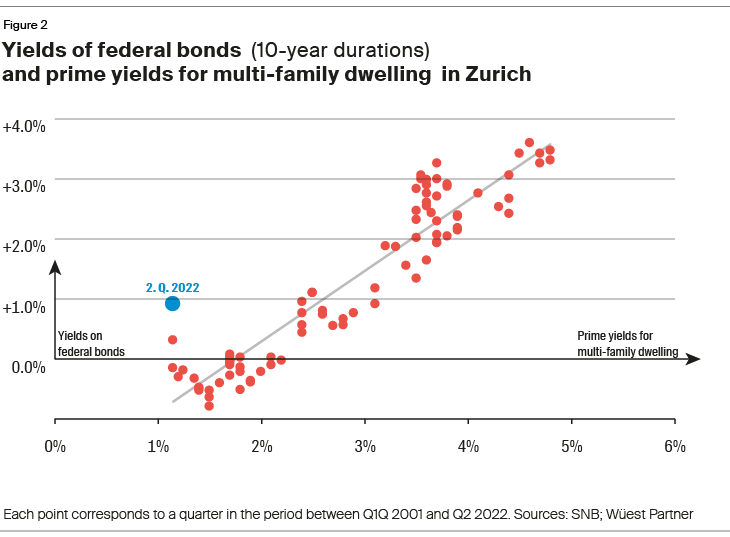

Government bond yields and real estate yields: a close correlation

Figure 2 compares 10-year federal bond yields (vertical axis) with the prime yields of multi-family dwelling (horizontal axis). Historically, these two measures have had a stable relationship, which is supported by the high correlation of 94 percent. The current situation, represented by the blue dot in Figure 2, thus represents a clear outlier.

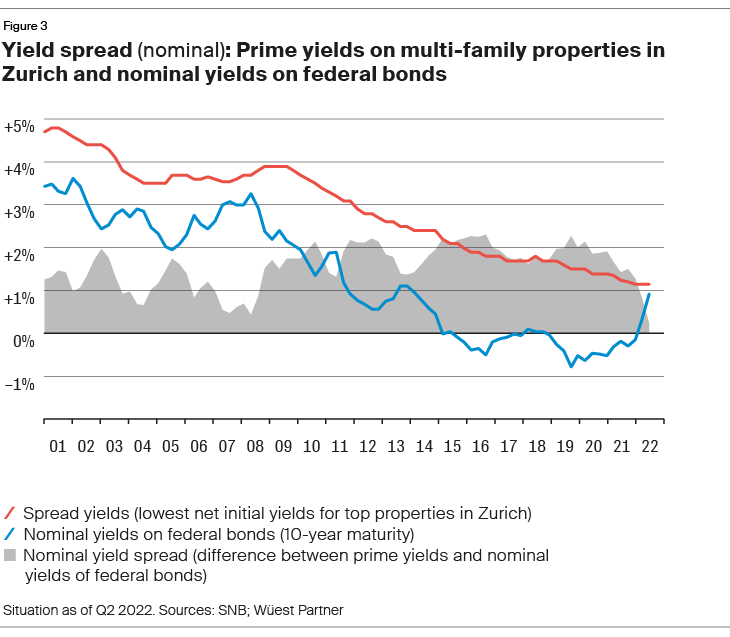

While the nominal yields on federal bonds have risen sharply over the year, the initial yields on Swiss investment properties have barely moved in 2022. As a result, the two ratios are closer than they have been for a long time, so that the risk premium for investments in real estate compared with federal bonds has virtually disappeared (see Fig. 3).

Nominal and real yield spreads

The difference between the yields on federal bonds and the initial yields on investment properties is defined as the spread. Even though interest rates have fallen steadily since the financial crisis in 2007/08, the yield spread between federal bonds and prime yields on multi-family properties in Zurich has always hovered around the 2 percent mark. This stability is partly due to the fact that initial yields react relatively sluggishly to macroeconomic changes. Moreover, the impact on initial yields depends on the duration and intensity of interest rate changes. In this millennium, interest rate rises have generally been temporary. Accordingly, the attractiveness of bonds as an investment alternative had already declined in each case, even before the entire real estate industry had adjusted to the higher interest rates. Currently, though, the nominal yield spread is practically zero, as shown in Figure 3.

However, if inflation is factored into bond yields, it becomes apparent that the yield spread is actually quite wide at present: the difference between the yields on federal bonds after deducting inflation expectations and prime yields on multi-family properties in Zurich is currently over 3 percentage points, which is a relatively high figure by historical standards (Fig. 4). Thus, the question arises: Where are real estate yields heading now?

Figure 5 takes a look at past dynamics, showing the quarterly change in federal bond yields and prime yields for multi-family properties in Zurich for each quarter since 2001. In Q2 2022 (blue dot), federal bond yields increased by almost 0.6 percentage points compared to the previous quarter, whereas net initial yields did not change. In figure 5, the correlation of -0.11 is significantly smaller than in figure 2, where the correlation of 0.94 refers to static data. This illustrates that expectations of returns on real estate investments are formed in the transaction market and cannot be derived purely mechanically from interest rate development. It is therefore important to take a comprehensive look at the investment market and the user market and to include them in the analyses; a quick glance at interest rates is not sufficient.

Outlook

The development of returns on investment properties is highly dependent on the evolution of inflation and interest rates. If real yields on federal bonds were to rise as well, real estate yields would probably follow suit (all else being equal). However, as long as inflation remains high, real yields on bonds will remain low. This, in turn, dampens the rise in expected returns on real estate investments. In this context, it is worth mentioning the (partial) inflation protection of real estate, which fixed-interest bonds such as government bonds lack. Both inflation and the increase in the reference interest rate can be partially passed on to residential properties.

In comparison to the recent peak in August, inflation is down 0.5 percentage points to 3.0 percent in October 2022. Yet, this is still well above the target range of 0-2 percent. There are currently many signs pointing to a definitive departure from negative interest rates and an even more restrictive monetary policy. With higher interest rates, the direction of initial yields on real estate is clear – it’s going namely upwards. However, the economic environment and the interplay between supply and demand also play an important role in the formation of real estate prices.