ESG-compliant real estate valuation — status quo and outlook

Published: April 18, 2021Last updated: January 6, 2026

Topics

With the Disclosure Regulation, the first important stage of European ESG regulation came into force on March 10. This makes sustainable real estate investments a concrete reality. The linchpin of investment decisions is the value of the investment. But how do ESG aspects affect valuation and what are the consequences for investors of ESG reporting of individual properties and portfolios? Rüdiger Hornung FRICS, Director at Wüest Partner Germany, provides an overview of the status quo and explains why data is a key component of ESG.

With the Disclosure Regulation, the first important stage of European ESG regulation came into force on March 10. This makes sustainable real estate investments a concrete reality. The linchpin of investment decisions is the value of the investment. But how do ESG aspects affect valuation and what are the consequences for investors of ESG reporting of individual properties and portfolios? Rüdiger Hornung FRICS, Director at Wüest Partner Germany, provides an overview of the status quo and explains why data is a key component of ESG.

In Europe, the Paris Climate Agreement resulted in the EU Action Plan for Sustainable Finance, which was presented in March 2018. This includes, among other things, the establishment of a uniform EU classification system (taxonomy) in which the term sustainability is defined. Furthermore, it provides for the creation of a label for green financial products based on this classification system as well as the clarification of the obligation of asset managers and institutional investors to take sustainability into account in investment processes and to implement disclosure requirements.

Sustainability is followed by ESG

At the national level, Germany already formulated the ambitious long-term goal of becoming largely climate-neutral by 2050 as part of its Climate Protection Plan 2050 in 2016. In 2018, the medium-term target was set to reduce greenhouse gas emissions by 38 percent by 2030. This explicitly includes the building sector. The regulatory instruments used to date to achieve this goal include the energy laws, which have been regularly tightened since 1977 and have also taken energy generation into account since the introduction of the Energy Saving Ordinance (EnEv), and the Renewable Energies Act (EEG).

The EU’s ESG Regulation expands the concept of sustainability that has prevailed to date from the level of the individual property to sustainable investment as a whole. This means that the focus is no longer only on the property itself, but also on the investor, who is held accountable. Programmatically, the aspect of ecological sustainability (E) remains largely intact and focuses on reducing CO2 emissions during the construction and operation of a property. In the area of social sustainability (S), the horizon of meaning of ESG goes beyond the aspect of user well-being considered so far and includes topics such as equality, inclusion and the observance of human rights. Economic sustainability, which has so far focused primarily on life cycle costs, is replaced by a governance term (G) that encompasses management structures, employee relations, and even compensation arrangements for employees and board members.

Status Quo

On March 10, 2021, the first part of the Disclosure Regulation came into force. As of this date, information on the sustainability of investment products must generally be provided in sales prospectuses, annual reports and on the homepages of KVGs, including for real estate investments.

The implementing provisions (Level 2) have not yet been specified and are not expected to be applied until the end of 2021. The same applies to the details of the taxonomy regulation, which is intended to make sustainability measurable in terms of the ESG criteria and will therefore primarily contain qualitative targets towards which a fund or investment should work. The objectives include, among others, the mitigation of climate change, the sustainable use and protection of water and marine resources, the shift to a circular economy (cradle-to-cradle), and the improvement of human and employee rights.

A technical expert group is tasked with establishing measurable criteria for the real estate sector. The specifications relate to the areas of construction, conversion and refurbishment, individual measures and services, as well as acquisition and holding periods. They are to come into force at the start of 2022.

ESG and sustainability in real estate valuation

How do ESG ratings actually affect the value of a property? First of all, there is no such thing as a “sustainable property is worth X percent more than a non-sustainable property” formula, and there won’t be one any time soon.

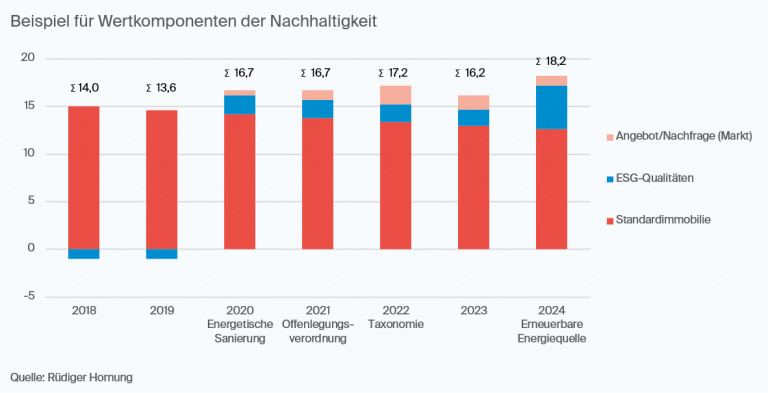

Basically, it can be stated that the added value of ESG or sustainability criteria can be reflected in two dimensions. On the one hand, in the property quality itself — the material used, the location, the design, resilience and flexibility. This can translate into good usability, low operating costs and a long remaining useful life, thus increasing the value of the property, regardless of a rating or certification. On the other hand, the transparency that a certificate or rating provides to market participants also influences market value. Due to the current low supply, the influence of sustainability may initially result in a high price premium, which could decrease as soon as the number of demonstrably sustainable properties on the market increases, and ultimately turn into a value discount for non-sustainable properties. A good ESG rating in combination with recognized proof would have become the standard at this point.

Data is the key

From the appraiser’s perspective, the data basis is always of the utmost importance in determining value. Here, standards are needed to ensure comparability, as well as technology to still be able to overview and evaluate the resulting data volumes. The classic BREEAM, LEED or DGNB sustainability certificates have already done excellent preliminary work with regard to the definition and measurability of the criteria. If such studies are available, they indicate an ecological claim, but the existence of a certification or rating alone is hardly a resilient variable for an evaluation. Rather, the question “What was certified when and, above all, with what result?” is decisive. The appraiser therefore needs as much building- and site-specific information as possible, for example CO2 emissions or infrastructure, in order to be able to make an assessment of the value impact that led to the certification result. Only this enables the appraiser to consider the individual quality criteria for the specific property in the multiple valuation parameters.

Therefore, the establishment of a standardized data framework is the basis for a meaningful ESG reporting as well as a real estate valuation. Relevant information must be collected, continuously supplemented and stored in a structured manner in a database to enable efficient evaluation for reporting and valuation. Setting up an information system for sustainability reporting can take up to two years, although digital tools simplify the process by, for example, importing certain parameters into the database via an app on a smartphone during each property inspection. Errors when transferring protocols are thus avoided and the data is immediately available.

In the presentation “ESG — No rating without data”, Rüdiger Hornung looks at practical examples of efficient data collection in the course of ESG reporting and explains, among other things, how the CO2 emissions of buildings can be calculated.

ESG-Rating

Wüest Partner carries out ESG ratings based on the EU taxonomy, which are based on ten indicators and 32 sub-indicators. With twelve sub-indicators, the largest proportion is in the environmental area. The parameters include primary energy demand in operations, waste management, structural compaction and the efficiency of technical equipment.

The social area in the ESG rating comprises ten sub-indicators, including public transport connections, pollution levels in the surrounding area and indoors, the quality of indoor and outdoor spaces, sound insulation and lighting situations.

Finally, the rating includes ten sub-indicators that address the governance aspect of sustainability. In addition to the classic indicator of life cycle costs, these also include the questions of the extent to which innovations are promoted, how pronounced stakeholder engagement is within the company, and whether the planning process has been transparent and participatory with the involvement of the population.

With the exception of the governance aspects, it is noticeable that most of the criteria have always been included in the course of a property valuation and taken into account in the valuation. It therefore makes sense to include and evaluate other ESG criteria during a property inspection for a valuation.

Measurability of CO2 emissions for individual properties and portfolios

The “E” in ESG, i.e., the ecological factors, is considered to have the greatest effect in relation to the long-term goal of climate neutrality by 2050. Reducing CO2 emissions through appropriate steps such as energy-efficient building refurbishment is therefore one of the most promising measures in the real estate industry. But how do you measure the emissions of a building, let alone an entire portfolio, in order to be able to evaluate the actual success through a before-and-after comparison? In terms of efficient calculation models, the industry is still at the beginning.

With the emissions and investment calculator, Wüest Partner already uses a specially developed tool that incorporates complex criteria into the calculation of a property’s ecological footprint. It enables investors and portfolio owners to keep an eye on the important CO2 indicator, to test scenarios of carbon-reducing measures for their efficiency, and to trace development paths of individual properties or portfolios alike.

Comparability and certification

In the course of the introduction of the ESG criteria, the need for information will increase further. At the same time, the question of data quality and integrity is coming to the fore. Who verifies the data and ensures that it is correct?

Here, thought should be given to the introduction of a neutral certification body that checks the evidence of the information brought into an ESG rating and ensures the quality of the results. This would hopefully spare the real estate industry an inglorious Volkswagen moment.